Hong Kong's Capital Markets Resurgence: Asia's Pre-eminent Financial Powerhouse

The Edge Singapore featured my article HK’S CAPITAL MARKETS RESURGENCE: ASIA’S PRE-EMINENT FINANCIAL POWERHOUSE on 13 October 2025.

Hong Kong's Capital Markets Resurgence: Asia's Pre-eminent Financial Powerhouse

The divergence between Hong Kong's struggling real economy and soaring capital markets reveals a fundamental shift in Asia's financial landscape.

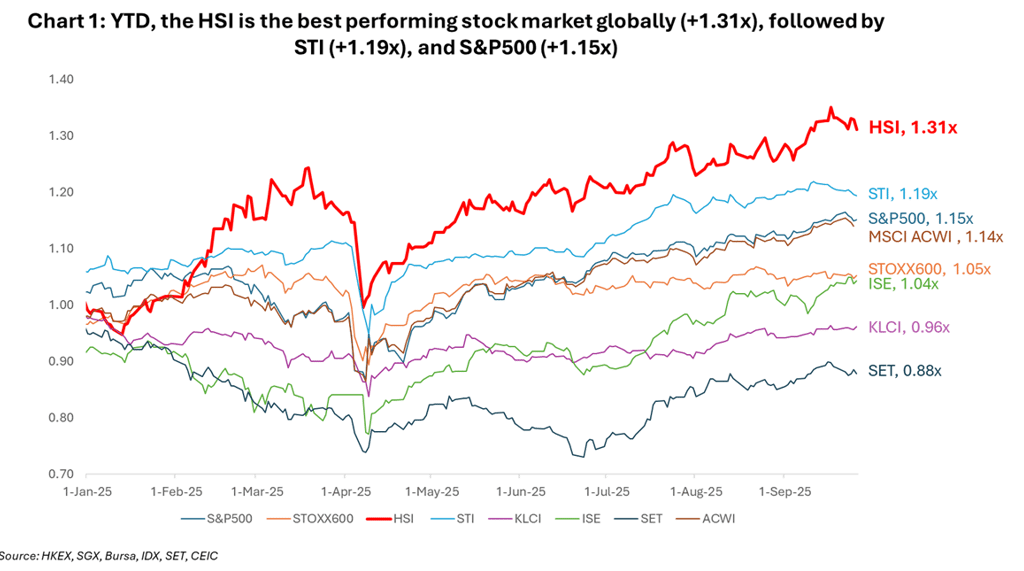

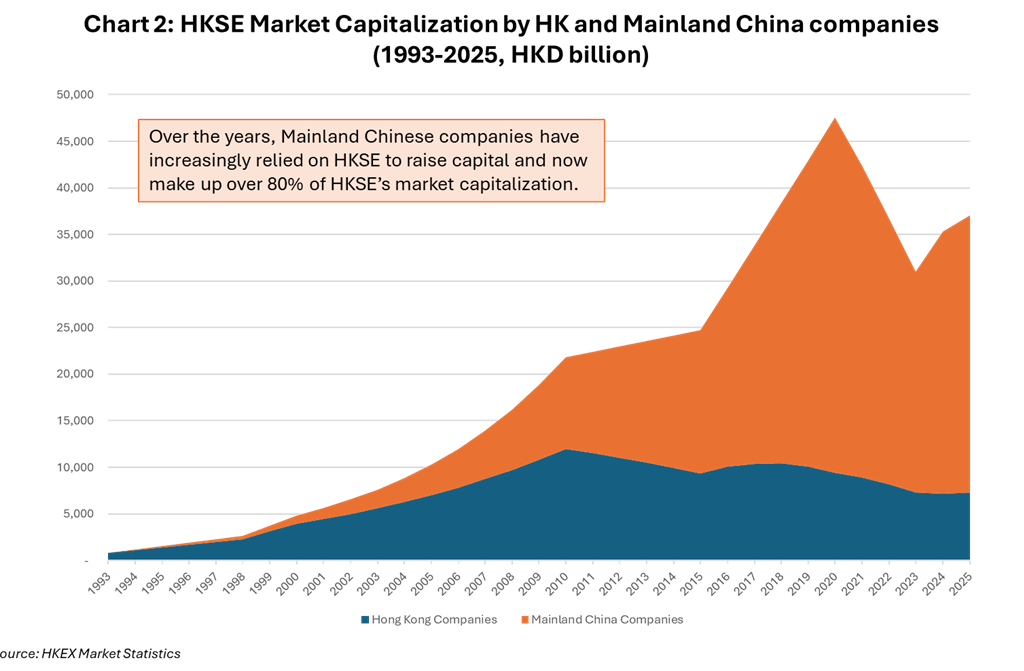

While Hong Kong's retail sales plunged 9.7% and property prices declined 7.1% in 2024, an extraordinary paradox emerged: the city's stock market delivered an 18% gain in 2024 and has grown by a further 26.6% year-to-date in 2025. With HK$107.1 billion (S$18.5 billion) raised in just the first half of 2025 – a sevenfold surge that left global competitors trailing far behind, Hong Kong has cemented its position as the world's top IPO destination in 2025.

This disconnect between economic fundamentals and capital market performance reveals a fundamental change. Hong Kong has evolved from a regional financial center serving diverse Asian economies into China's primary international capital gateway, fundamentally reshaping Asia's financial landscape and leaving regional competitors scrambling to find their niche.

The Great Divergence: Economy Versus Markets

Hong Kong's economic indicators paint a picture of persistent malaise. GDP growth remains weak at 2.5% for 2024, with forecasts suggesting only modest improvement to 2.3-2.5% in 2025. Retail consumption, historically the backbone of Hong Kong's service economy, contracted sharply, with December 2024 retail sales at just 73.1% of pre-pandemic levels. The property sector, long considered the economy's cornerstone, saw prices fall to 2012 levels in inflation-adjusted terms.

Yet amid this economic decline, Hong Kong's capital markets experienced a dramatic turnaround. The Hang Seng Index (HSI) surged 26.6% year-to-date through September 2025 ranks among the world's best-performing major indices. Daily trading volumes surged 118% to HK$240.2 billion (S$41.4 billion), while ETF turnover jumped 184% to HK$33.8 billion (S$5.85 billion). Hong Kong Exchanges and Clearing posted record profits of HK$8.52 billion (S$1.5 billion) in the first half of 2025, representing 39% growth year-on-year.

The driver behind this extraordinary disconnect is Beijing's strategic recalibration. Rather than allow market forces to determine Hong Kong's role, Chinese authorities have explicitly designated the city as the primary offshore fundraising hub for "China Inc.", a structural policy pivot that transforms Hong Kong from a diversified regional center into China's dedicated international capital gateway.

Beijing's Master Stroke: Policy-Driven Market Dominance

The transformation stems from five interconnected policy decisions that collectively redirect China's capital flows through Hong Kong.

First, Beijing curtailed US-bound IPO approvals while streamlining Hong Kong listings. Chinese regulators now process A+H dual listings in just 30 business days for qualified applicants, compared to lengthy and uncertain US approval processes. The result: 47 new A+H listing applications in the first half of 2025 versus just five in all of 2024.

Second, capital flow restrictions were systematically relaxed. The China Securities Regulatory Commission (CSRC) increased the Mutual Recognition of Funds sales cap from 50% to 80%, enabling 60% more mainland investment into Hong Kong funds. Wealth Management Connect 2.0 facilitated RMB 16 billion (S$3.1 billion) in mainland investment flows by June 2025, nearly tripling previous volumes.

Third, Beijing positioned Hong Kong as the preferred venue for strategic sector listings. Companies in artificial intelligence, new energy, semiconductors, healthcare, and advanced manufacturing, sectors central to China's economic strategy, are actively encouraged to seek Hong Kong listings. These sectors represented a significant portion of H1 2025 IPO proceeds.

Fourth, geopolitical pressure provided additional momentum. Escalating US-China tensions and tightening US regulations on Chinese firms made Hong Kong's autonomy and international status crucial for capital access. "Homecoming" listings by major Chinese companies previously listed in the US, including technology giants such as Alibaba, JD.com and Baidu, have reinforced this trend.

Fifth, mainland investor participation surged through Stock Connect mechanisms. Mainland investors now contribute 50% of Hong Kong's daily stock turnover, up from 30% at the beginning of 2024. Southbound trading volumes nearly doubled, reaching HK$112.0 billion (S$19.3 billion) in average daily turnover.

The Numbers Behind the Renaissance

The statistics underlying Hong Kong's capital market dominance are staggering. IPO fundraising of HK$107.1 billion (S$18.5 billion) in the first half of 2025 exceeded most exchanges' full-year totals, positioning Hong Kong as the global leader in new listing proceeds. Over 200 companies are in the active IPO pipeline, including a record 210 Main Board applications, more than doubled from 86 applicants at end-2024.

Trading activity reached unprecedented levels. The exchange's average daily turnover of HK$240.2 billion (S$41.4 billion) covered half of HKEX's top ten trading days in previous years. Leveraged and inverse products saw 75% growth in daily turnover to HK$4.2 billion (S$0.7 billion), while securities surged 78% to HK$9.6 billion (S$1.7 billion) daily.

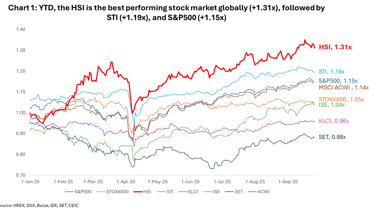

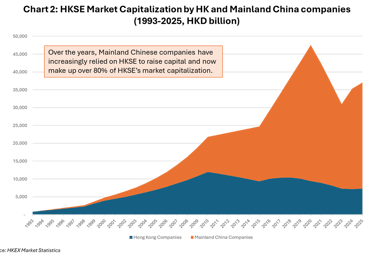

Most significantly, mainland companies now dominate Hong Kong's market composition. Chinese enterprises represent 1,478 of 2,631 total listings (56% by count) but command nearly 80% of market capitalization due to their substantially larger scale. This concentration has fundamentally altered Hong Kong's risk-return profile, making it essentially a leveraged play on China's economic performance rather than a diversified regional market.

Regional Implications: An Unbridgeable Gulf

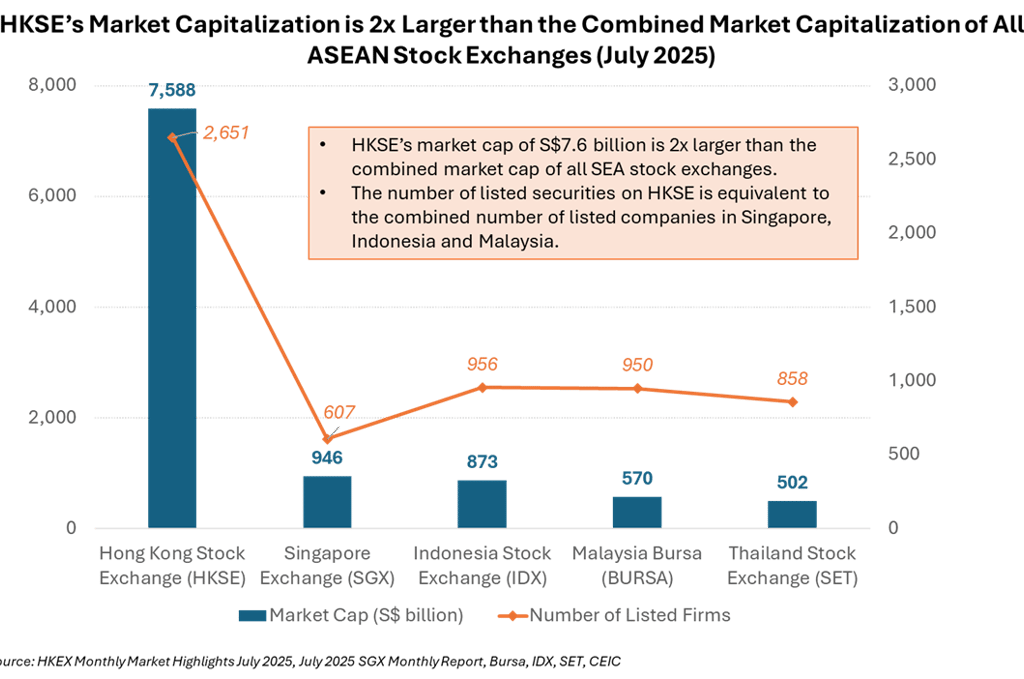

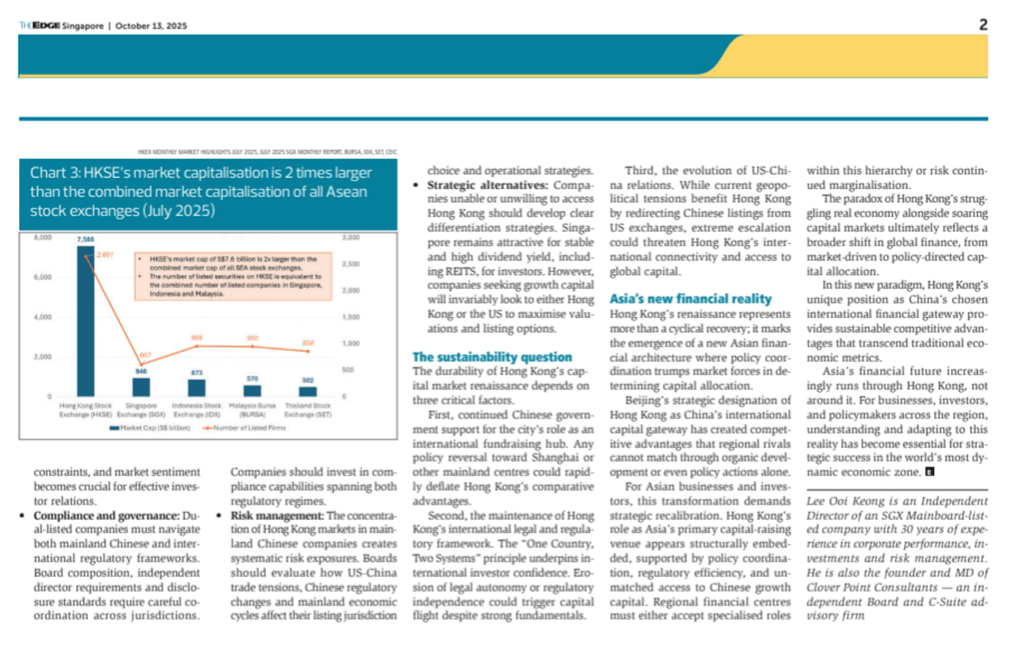

The scale differential between Hong Kong and Southeast Asian exchanges has become virtually unbridgeable. Hong Kong's market capitalization of HK$42.7 trillion (S$7.4 trillion) in H1 2025 exceeds the combined capitalization of all ASEAN exchanges by approximately twofold. Daily trading volumes reveal an even starker disparity: Hong Kong's HK$240.2 billion (S$41.4 billion) dwarfs Singapore's S$1.2 billion (equivalent to HK$7.0 billion) by a factor of 34 times.

The IPO comparison is particularly revealing. Hong Kong's first-half 2025 fundraising of HK$107.1 billion (S$18.5 billion) compares to Southeast Asia's entire regional total of just S$1.89 billion (approximately HK$10.9 billion) for the same period – a differential of nearly 10:1. In contrast, Singapore saw only five new listings as at July 2025 against Hong Kong's 42 in H1 2025.

This disparity reflects fundamental structural advantages rather than cyclical factors. Hong Kong benefits from Beijing's explicit policy support, while ASEAN markets depend on organic regional growth and voluntary cooperation initiatives that have historically proven difficult to implement. The ASEAN Trading Link, launched in 2012, connected only three markets despite ten years of effort and was eventually decommissioned in 2017 due to limited adoption and political barriers.

Current ASEAN initiatives show modest promise. The Depository Receipts Programme launched in November 2024 has enabled cross-listings between Singapore and Thailand, while the ASEAN-Interconnected Sustainability Ecosystem promotes common ESG standards. However, these building-block approaches lack the comprehensive, government-backed coordination that drives Hong Kong's dominance.

Strategic Implications for Asian Markets

Hong Kong's transformation carries direct implications for regional financial landscape. The city's evolution into China's dedicated international capital gateway means other Asian financial centers must either find differentiated niches or accept secondary roles.

Singapore faces the most direct competitive pressure. While maintaining advantages in wealth management, ASEAN market access, and regulatory innovation, Singapore cannot replicate Hong Kong's exclusive access to Chinese growth capital. The MAS EQDP fund of S$5 billion, even with 1:1 co-investment ratios, represents only 1.1% of SGX's total market capitalization – insufficient to move markets meaningfully.

Malaysia, Thailand, and Indonesia compete primarily on domestic economic fundamentals rather than regional financial hub aspirations. Malaysia's bursa recorded 48% more listings and 109% higher IPO proceeds in the first half of 2025, while Indonesia nearly doubled IPO proceeds despite election uncertainty. However, their combined market influence remains marginal compared to Hong Kong's gravitational pull.

Vietnam presents a unique case. With US$150 billion market capitalization and 9.2% gains in August 2025, it offers compelling growth opportunities for investors seeking exposure to frontier manufacturing and young demographics. Yet Vietnam's capital market infrastructure remains underdeveloped relative to its economic potential.

Board Director and Corporate Implications

For board directors and senior executives across Asia, Hong Kong's dominance creates both opportunities and strategic imperatives.

Capital Access Strategy: Companies seeking substantial growth capital will default to Hong Kong listings, particularly for technology, biotech, healthcare and industrial sectors favored by Chinese policy. The A+H dual listing structure provides optimal access to both domestic and international investor bases, with regulatory approval timelines now competitive with other major exchanges. Already, Singapore biotech startups such as Mirxes prefer to list in Hong Kong than suffer a valuation discount on the SGX.

Investor Base Considerations: Hong Kong-listed companies should prepare for increasingly mainland-dominated shareholding structures. With mainland investors comprising 50% of daily turnover, understanding Chinese institutional investment patterns, regulatory constraints, and market sentiment becomes crucial for effective investor relations.

Compliance and Governance: Dual-listed companies must navigate both mainland Chinese and international regulatory frameworks. Board composition, independent director requirements and disclosure standards require careful coordination across jurisdictions. Companies should invest in compliance capabilities spanning both regulatory regimes.

Risk Management: The concentration of Hong Kong markets in mainland Chinese companies creates systematic risk exposures. Boards should evaluate how US-China trade tensions, Chinese regulatory changes and mainland economic cycles affect their listing jurisdiction choice and operational strategies.

Strategic Alternatives: Companies unable or unwilling to access Hong Kong should develop clear differentiation strategies. Singapore remains attractive for stable and high dividend yield, including REITS, investors. However, companies seeking growth capital will invariably look to either Hong Kong or US to maximize valuations and listing options.

The Sustainability Question

The durability of Hong Kong's capital market renaissance depends on three critical factors. First, continued Chinese government support for the city's role as international fundraising hub. Any policy reversal toward Shanghai or other mainland centers could rapidly deflate Hong Kong's comparative advantages.

Second, the maintenance of Hong Kong's international legal and regulatory framework. The "One Country, Two Systems" principle underpins international investor confidence. Erosion of legal autonomy or regulatory independence could trigger capital flight despite strong fundamentals.

Third, the evolution of US-China relations. While current geopolitical tensions benefit Hong Kong by redirecting Chinese listings from US exchanges, extreme escalation could threaten Hong Kong's international connectivity and access to global capital.

Conclusion: Asia's New Financial Reality

Hong Kong's renaissance represents more than a cyclical recovery; it marks the emergence of a new Asian financial architecture where policy coordination trumps market forces in determining capital allocation. Beijing's strategic designation of Hong Kong as China's international capital gateway has created competitive advantages that regional rivals cannot match through organic development or even policy actions alone.

For Asian businesses and investors, this transformation demands strategic recalibration. Hong Kong's role as Asia's primary capital-raising venue appears structurally embedded, supported by policy coordination, regulatory efficiency, and unmatched access to Chinese growth capital. Regional financial centers must either accept specialized roles within this hierarchy or risk continued marginalization.

The paradox of Hong Kong's struggling real economy alongside soaring capital markets ultimately reflects a broader shift in global finance, from market-driven to policy-directed capital allocation. In this new paradigm, Hong Kong's unique position as China's chosen international financial gateway provides sustainable competitive advantages that transcend traditional economic metrics.

Asia's financial future increasingly runs through Hong Kong, not around it. For businesses, investors, and policymakers across the region, understanding and adapting to this reality has become essential for strategic success in the world's most dynamic economic zone.

Written by:

Lee Ooi Keong

28 September 2025

Brief bio: Lee Ooi Keong is an Independent Director of a SGX Mainboard-listed company with 30-years of experience in corporate performance, investments and risk management. He is also the founder and MD of Clover Point Consultants – an independent Board and C-Suite advisory firm.