Independent Board Advisory, Executive Education and Professional Speaking

Revitalising Singapore's Equity Market: What the MAS package fixes and doesn't

The Edge Singapore featured my article "Revitalising Singapore's Equity Market: What the MAS package fixes and doesn't" on 2 March 2026.

Lee Ooi Keong

3/10/202613 min read

Revitalising Singapore's Equity Market: What the MAS Package Fixes and Doesn't

Singapore's equity market staged a convincing rally in 2025. The Straits Times Index (STI) rose 22.7%, turnover surged 21% to nearly S$1.5 billion daily, and IPO proceeds reached US$2.5 billion, a forty-fold jump from 2024's dismal US$64 million. These numbers seemed to vindicate the Monetary Authority of Singapore (MAS)'s reform package, expanded to S$6.5 billion in Budget 2026.

Yet trading data tells a more complicated story.

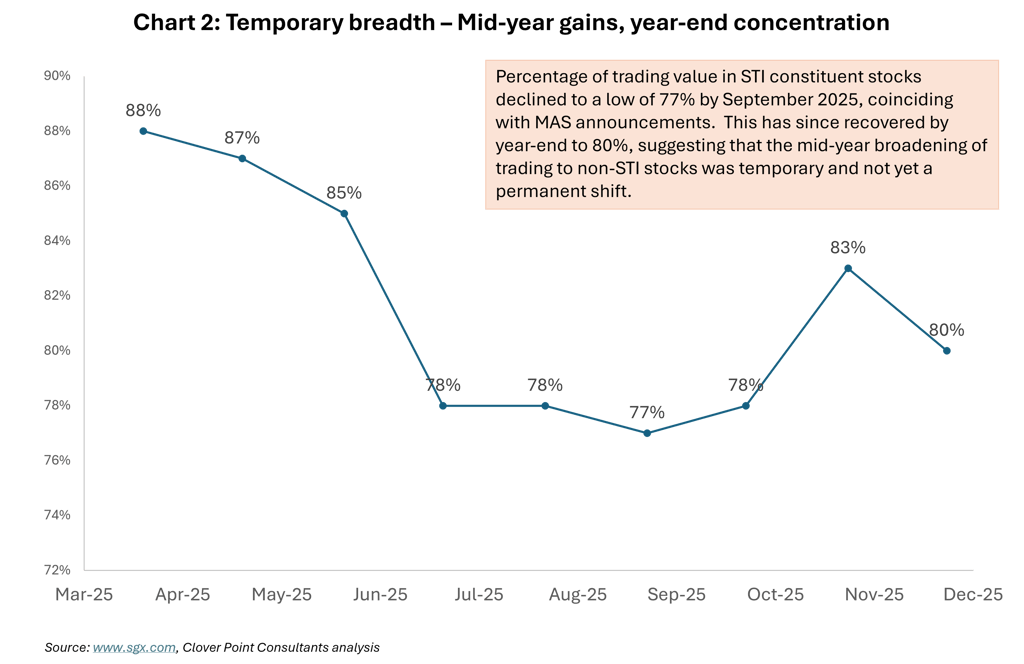

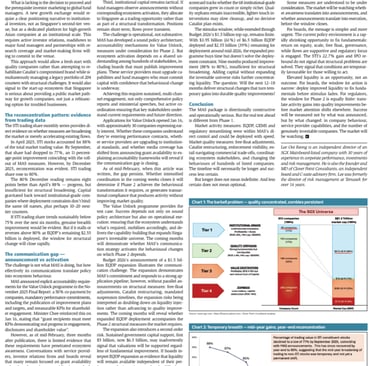

STI stocks commanded 88% of total market trading value in April 2025. By September, that share had dropped to 77% as breadth improved mid-year. But by December, it had reconcentrated to 80%. The pattern suggests MAS's measures created temporary broadening that did not hold – liquidity accelerated, but did not durably redistribute beyond the market's established apex.

For boards and institutional investors, this raises a fundamental question: Is success defined by market activity; higher turnover, tighter spreads, more IPOs, or by market quality: expanding the number of companies worth owning at institutional scale?

The distinction matters, because the two definitions lead to very different verdicts on whether Singapore's equity market is being revitalised or merely made busier.

The Two Scorecards – Activity vs Quality

The MAS package explicitly embraces "flywheel" logic: improve liquidity and infrastructure first, then listings and valuations follow. This creates two distinct success metrics that must be assessed separately.

Market activity encompasses what MAS can directly influence within 12 to 18 months: trading value and velocity; breadth beyond STI constituents; research coverage; IPO efficiency; retail access costs; and cross-border connectivity.

Market quality comprises outcomes MAS can only indirectly influence over the long term: the number of companies meeting institutional investability thresholds; average market capitalisation and free float for mid-sized companies; reduction of loss-making and suspended counters; whether Catalist becomes a credible growth pipeline; and how quickly suspended companies are resolved.

The focus on market activity first may reflect deliberate sequencing. The question is whether this phased approach will translate to decisive action on quality with clear timelines, or whether momentum will dissipate once stimulus fades.

Why does this distinction matter? The 2025 rally demonstrated that markets can surge on liquidity while fundamentals remain structurally weak beneath the indices.

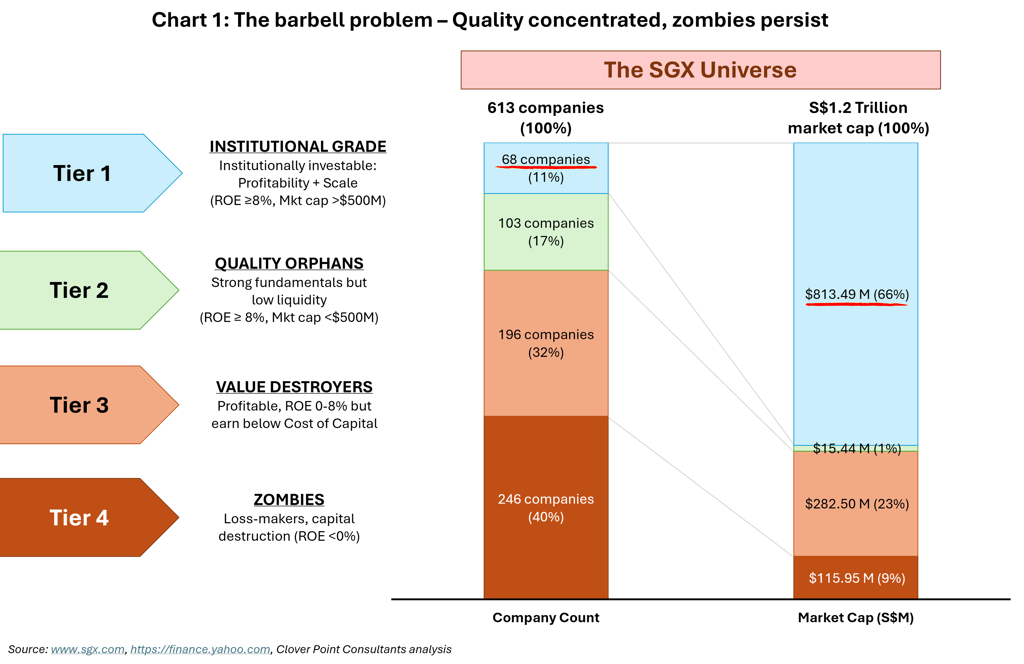

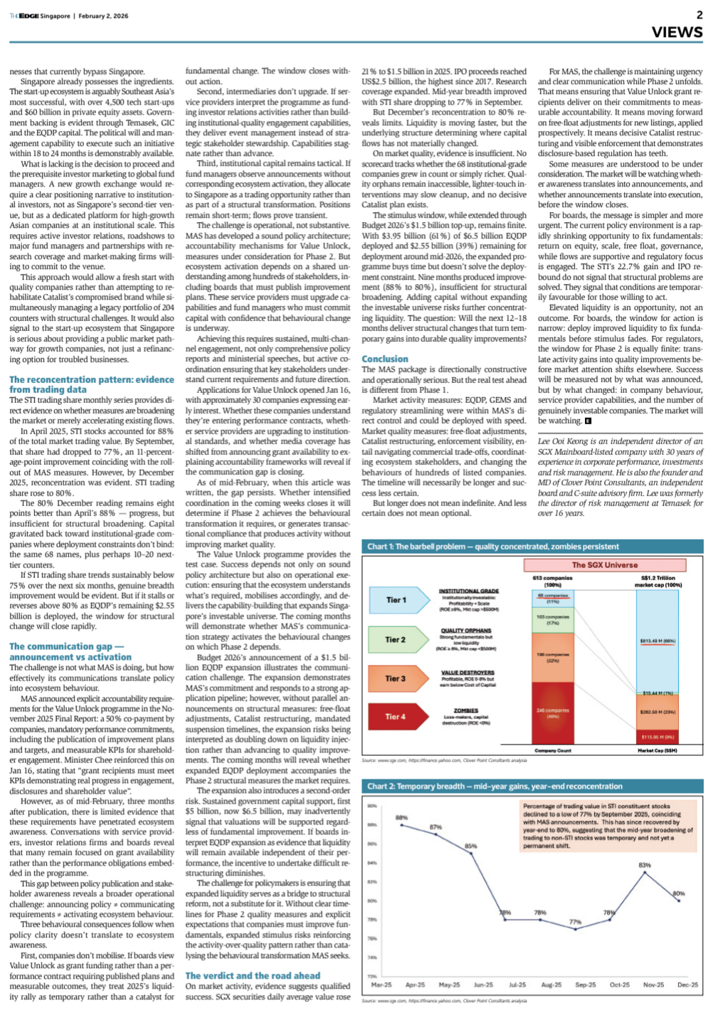

Bottom-up analysis of SGX's 613 listed companies reveals a barbell market. At one end sit 68 Tier 1 Institutional-Grade companies (11% of listings with return on equity (ROE) of at least 8% and market cap above S$500 million) holding S$813.5 billion or 66% of total market cap. These are the counters that meet institutional mandates for size, liquidity and profitability.

At the other end sit Tier 4 Zombies, 246 loss-making companies (40% of listings) holding S$116 billion or 9% of market cap. This tier includes 48 suspended counters.

In between lies a hollow middle: 299 companies holding just 24% of market cap. This includes 103 Tier 2 Quality Orphans, companies earning ROE above 8% but averaging only S$150 million market cap, too small for institutional mandates, and 196 Tier 3 Value Destroyers earning positive accounting profits but ROE below cost of equity.

The risk is declaring victory on market activity; higher turnover, more IPOs, tighter spreads, while market quality remains unchanged. That would mistake higher trading volumes for a genuinely broader investable market.

Demand Measures: EQDP, GIP, GEMS – Reinforcing Existing Patterns

The Equity Market Development Programme (EQDP), expanded in Budget 2026 from S$5 billion to S$6.5 billion, represents the package's most direct liquidity lever. By mid-February 2026, S$3.95 billion had been allocated across nine asset managers, with further tranches targeting the remaining S$2.55 billion expected around mid-2026.

This addresses a chronic gap: only approximately S$20 billion is invested through Singapore-focused funds (0.5% of the S$4 trillion AUM domiciled in Singapore), insufficient to support 613 listed companies.

Yet even S$6.5 billion represents less than 0.6% of SGX's approximately S$1.1 trillion market capitalisation and less than five days of average daily trading value. More critically, expanding the programme from S$5 billion to S$6.5 billion extends the stimulus runway but doesn't resolve the fundamental deployment constraint.

More critically, EQDP faces a deployment constraint that has not been publicly addressed. Tier 2 Quality Orphans average S$150 million market cap with likely 10 to 20% free float, yielding S$15 to 30 million in available float per company. Yet institutional mandates typically require minimum position sizes of roughly ~S$30 million for smaller family offices and S$200 million or more for larger institutional investors.

Large EQDP pools cannot deploy into quality orphans without overwhelming available float or generating excessive price impact. Capital naturally flows to institutional-grade companies averaging S$12 billion market cap, where ample float exists. This improves liquidity where it already existed but does nothing to expand the number of genuinely investable companies.

Similarly, the Global Investor Programme adjustment requires S$50 million of family office assets to be deployed in Singapore-listed equities, but these S$50 million deployments flow overwhelmingly to liquid large-cap stocks.

Grant for Equity Market Singapore (GEMS) enhancements improved research coverage (funding per report: S$4,000→S$6,000; firms: 14→22; monthly reports: 39→50), helping price discovery. But research cannot solve the binding constraint: at S$150 million market cap and limited free float, available float sits below institutional minimums.

Supply and Regulatory Measures: Streamlining and Tighter Oversight

MAS and SGX RegCo have committed to completing listing reviews within six to eight weeks under ordinary circumstances, consolidating review functions with SGX RegCo, and streamlining qualitative admission criteria. These reduce friction and should improve time-to-market for prospective issuers.

The critical qualifier is that disclosure-based regimes only work if enforcement is credible and visible. MAS has signaled it will adopt a tighter enforcement posture. The question is whether this translates to visible, swift actions that rebuild investor confidence. As of early 2026, no enforcement statistics or case outcomes have been disclosed.

Post-listing interventions were softened: SGX removed the financial watchlist, shifted to private queries, and narrowed suspensions to going-concern cases. This reduces disruption but raises market quality concerns – softening interventions without tightening resolution timelines risks appearing as cosmetics over hygiene.

48 counters holding S$2.8 billion remain suspended with no mandated resolution timelines. Two companies have been suspended for over a decade since November 2015 with no resolution dates.

The S$30 million Value Unlock programme provides grants for investor relations and strategy capabilities with explicit performance requirements. Announced in November 2025 and opened for applications in January 2026, the programme requires 50% co-payment from companies and mandates measurable commitments: participation in investor engagements, publication of improvement plans and targets, and public disclosure of progress. Effectiveness will depend on whether companies treat this as a performance contract that drives genuine capability building, rather than a subsidy.

The Nasdaq Bridge – Crown Jewels Only

The SGX-Nasdaq dual listing bridge targets: S$2bn+ market cap (mid-2026 launch) reduces cross-border friction for institutional-grade companies but may cannibalize capital from smaller and mid-tier stocks.

More concerning is liquidity risk. If global investors trade primarily on Nasdaq given deeper liquidity, tighter spreads and 24-hour access, Singapore becomes a symbolic venue. This would worsen concentration. Institutional capital would cluster around the handful of dual-listed stocks and STI constituents that dominate trading, further marginalising smaller companies.

Market-making incentives for 'small- and mid-cap stocks outside the STI' are expected in Q1 2026, but dual-listed stock commitments during Singapore hours remain under consideration. The challenge: ensuring Singapore doesn't become an afterthought in its own dual listings.

The Free Float Question: Deferred, Not Forgotten

The free float constraint remains unaddressed at this stage. Singapore's 10% minimum compares to 25% in Hong Kong and Bursa Malaysia. SGX notes that 75% of issuers exceed 20% free float, but this statistic includes institutional-grade companies and hides the problem facing Quality Orphans where low free float blocks institutional access.

The problem compounds: as discussed earlier, even higher free float percentages won't create enough dollar value for institutional investors to build meaningful positions in quality orphans.

Market observers suggest free float adjustments may be under consideration for future phases. One possible workaround is to apply higher float requirements similar to regional benchmarks only to new listings from 2027 onwards. Existing listed companies would be grandfathered thus avoiding forced sell-downs and prices pressures while prospectively fixing the constraint that keeps quality orphans institutionally inaccessible.

The Catalist Problem – Rehabilitation House, Not Growth Pipeline

Catalist holds 204 counters, one-third of SGX's listings, yet represents approximately 1% of total market cap, with only 41% profitable. The board was designed as a growth pipeline for ambitious mid-market companies. Instead, it has become a rehabilitation house for struggling businesses and failed Mainboard graduates.

The evidence is stark: 17 companies demoted from Mainboard to Catalist over the past decade, while only nine graduated upward (several subsequently faltering). The net flow is downward, signaling Catalist has lost credibility as a pathway to institutional-grade status.

No decisive restructuring plan has been implemented, and the board remains under review with no announced timeline. Yet the problem is becoming more acute as the board accumulates legacy names with limited growth prospects while consuming regulatory resources and occupying valuable exchange real estate.

One possibility worth considering: let Catalist wind down naturally while establishing a new, properly curated growth exchange exclusively targeting high-growth companies from not only Singapore but also the entire Asian startup ecosystem, backed by government-linked capital and including Nasdaq Global Listing Board dual-listed candidates and promising high-growth listed companies on the Mainboard.

This exchange would focus on growth metrics (revenue trajectories, market expansion, capital efficiency) rather than profitability thresholds, providing a credible pathway for technology companies, fintech firms, and regional growth businesses that currently bypass Singapore.

Singapore already possesses the ingredients. The startup ecosystem is arguably Southeast Asia's most successful, with over 4,500 tech startups and S$60 billion in private equity assets. Government backing is evident through Temasek, GIC and the EQDP capital. The political will and management capability to execute such an initiative within 18 to 24 months is demonstrably available.

What is lacking is the decision to proceed and the prerequisite investor marketing to global fund managers. A new growth exchange would require a clear positioning narrative to institutional investors, not as Singapore's second-tier venue, but as a dedicated platform for high-growth Asian companies at institutional scale. This requires active investor relations, roadshows to major fund managers and partnerships with research coverage and market-making firms willing to commit to the venue.

This approach would allow a fresh start with quality companies rather than attempting to rehabilitate Catalist's compromised brand while simultaneously managing a legacy portfolio of 204 counters with structural challenges. It would also signal to the startup ecosystem that Singapore is serious about providing a public market pathway for growth companies, not just a refinancing option for troubled businesses.

The Reconcentration Pattern: Evidence from Trading Data

The STI trading share monthly series provides direct evidence on whether measures are broadening the market or merely accelerating existing flows.

In April 2025, STI stocks accounted for 88% of total market trading value. By September, that share had dropped to 77%, an 11-percentage-point improvement coinciding with the rollout of MAS measures. Yet by December, reconcentration was evident. STI trading share rose to 80%.

The 80% December reading remains 8 points better than April's 88% – progress, but insufficient for structural broadening. Capital gravitated back toward institutional-grade companies where deployment constraints don't bind: the same 68 names, plus perhaps 10-20 next-tier counters.

If STI trading share trends sustainably below 75% over the next six months, genuine breadth improvement would be evident. But if it stalls or reverses above 80% as EQDP's remaining S$2.55 billion is deployed, the window for structural change will close rapidly.

The Communication Gap – Announcement vs. Activation

The challenge is not what MAS is doing but how effectively their communications are translating policy into ecosystem behavior.

MAS announced explicit accountability requirements for the Value Unlock programme in the November 2025 Final Report: 50% co-payment from companies, mandatory performance commitments including publication of improvement plans and targets, and measurable KPIs for shareholder engagement. Minister Chee reinforced this on January 16, 2026, stating that "grant recipients must meet KPIs demonstrating real progress in engagement, disclosures and shareholder value."

Yet as of mid-February 2026, three months after publication, limited evidence suggests these requirements have penetrated ecosystem awareness. Conversations with service providers, investor relations firms and boards reveal that many remain focused on grant availability rather than the performance obligations embedded in the programme.

This gap between policy publication and stakeholder awareness reveals a broader operational challenge: announcing policy ≠ communicating requirements ≠ activating ecosystem behavior.

Three behavioral consequences follow when policy clarity doesn't translate to ecosystem awareness.

First, companies don't mobilize. If boards view Value Unlock as grant funding rather than a performance contract requiring published plans and measurable outcomes, they treat 2025's liquidity rally as temporary rather than a catalyst for fundamental change. The window closes without action.

Second, intermediaries don't upgrade. If service providers interpret the programme as funding investor relations activities rather than building institutional-quality engagement capabilities, they deliver event management instead of strategic stakeholder stewardship. Capabilities stagnate rather than advance.

Third, institutional capital remains tactical. If fund managers observe announcements without corresponding ecosystem activation, they allocate to Singapore as a trading opportunity rather than a structural transformation. Positions remain short-term; flows prove transient.

The challenge is operational, not substantive. MAS has developed sound policy architecture; accountability mechanisms for Value Unlock, measures under consideration for Phase 2. But ecosystem activation depends on shared understanding across hundreds of stakeholders: boards who must publish improvement plans, service providers who must upgrade capabilities, fund managers who must commit capital with confidence that behavioral change is underway.

Achieving this requires sustained, multi-channel engagement, not only comprehensive policy reports and ministerial speeches, but active coordination ensuring that key stakeholders understand current requirements and future direction.

Applications for Value Unlock opened January 16, with approximately 30 companies expressing early interest. Whether these companies understand they're entering performance contracts, whether service providers are upgrading to institutional standards, and whether media coverage has shifted from announcing grant availability to explaining accountability frameworks will reveal if the communication gap is closing.

As of mid-February 2026, when this article was written, the gap persists. Whether intensified coordination in coming weeks closes it, will determine if Phase 2 achieves the behavioral transformation it requires, or generates transactional compliance that produces activity without improving market quality.

The Value Unlock programme provides the test case. Success depends not only on sound policy architecture, but on operational execution: ensuring that the ecosystem understands what's required, mobilizes accordingly, and delivers the capability building that expands Singapore's investable universe. The coming months will demonstrate whether MAS's communication strategy activates the behavioral changes Phase 2 depends on.

Budget 2026's announcement of a S$1.5 billion EQDP expansion illustrates the communication challenge. The expansion demonstrates MAS's commitment and responds to strong application pipeline. Yet without parallel announcements on structural measures: free float adjustments, Catalist restructuring, mandated suspension timelines, the expansion risks being interpreted as doubling down on liquidity injection rather than advancing to quality improvements. The coming months will reveal whether expanded EQDP deployment accompanies the Phase 2 structural measures the market requires.

The expansion also introduces a second-order risk. Sustained government capital support, first S$5 billion, now S$6.5 billion, may inadvertently signal that valuations will be supported regardless of fundamental improvement. If boards interpret EQDP expansion as evidence that liquidity will remain available independent of their performance, the incentive to undertake difficult restructuring diminishes.

The challenge for policymakers is ensuring that expanded liquidity serves as a bridge to structural reform, not a substitute for it. Without clear timelines for Phase 2 quality measures and explicit expectations that companies must improve fundamentals, expanded stimulus risks reinforcing the activity-over-quality pattern rather than catalyzing the behavioral transformation MAS seeks.

The Verdict and the Road Ahead

On market activity, evidence suggests qualified success. SGX securities daily average value rose 21% to S$1.5 billion in 2025. IPO proceeds reached US$2.5 billion, the highest since 2017. Research coverage expanded. Mid-year breadth improved with STI share dropping to 77% in September.

But December's reconcentration to 80% reveals limits. Liquidity is moving faster, but the underlying structure determining where capital flows has not materially changed.

On market quality, evidence is insufficient. No scorecard tracks whether the 68 institutional-grade companies grew in count or simply richer. Quality orphans remain inaccessible, lighter-touch interventions may slow cleanup, and no decisive Catalist plan exists.

The stimulus window, while extended through Budget 2026's S$1.5 billion top-up, remains finite. With S$3.95 billion (61%) of S$6.5 billion EQDP deployed and S$2.55 billion (39%) remaining for deployment around mid-2026, the expanded programme buys time but doesn't solve the deployment constraint. Nine months produced improvement (88%→80%) insufficient for structural broadening. Adding capital without expanding the investable universe risks concentrating liquidity further. The question: will the next 12-18 months deliver structural changes that turn temporary gains into durable quality improvements?

Conclusion

The MAS package is directionally constructive and operationally serious. But the real test ahead is different from Phase 1.

Market activity measures: EQDP, GEMS, regulatory streamlining, were within MAS's direct control and could be deployed with speed. Market quality measures: free float adjustments, Catalist restructuring, enforcement visibility, entails navigating commercial trade-offs, coordinating ecosystem stakeholders, and changing behaviors of hundreds of listed companies. The timeline will necessarily be longer and success less certain.

But longer does not mean indefinite. And less certain does not mean optional.

For MAS, the challenge is maintaining urgency and clear communication while Phase 2 unfolds. That means ensuring Value Unlock grant recipients deliver measurable accountability as committed. It means moving forward on free float adjustments for new listings, applied prospectively. It means decisive Catalist restructuring and visible enforcement that demonstrates disclosure-based regulation has teeth.

Some measures are understood to be under consideration. The market will be watching whether awareness translates to announcements, and announcements to execution, before the window closes.

For boards, the message is simpler and more urgent. The current policy environment is a rapidly shrinking opportunity to fix fundamentals: return on equity, scale, free float, governance, while flows are supportive and regulatory focus is engaged. The STI's 22.7% gain and IPO rebound do not signal that structural problems are solved. They signal that conditions are temporarily favorable for those willing to act.

Elevated liquidity is an opportunity, not an outcome. For boards, the window for action is narrow: deploy improved liquidity to fix fundamentals before stimulus fades. For regulators, the window for Phase 2 is equally finite: translate activity gains into quality improvements before market attention shifts elsewhere. Success will be measured not by what was announced, but by what changed: in company behavior, service provider capabilities, and the number of genuinely investable companies. The market will be watching.

Written by:

Lee Ooi Keong

16 February 2026

Brief bio: Lee Ooi Keong is an Independent Director of a SGX Mainboard-listed company

with 30-years of experience in corporate performance, investments and risk management. He is also the founder and MD of Clover Point Consultants – an independent Board and C-Suite advisory firm. Ooi Keong was formerly a Director of Risk Management in Temasek for over 16 years.