Singapore's Energy Vulnerability Paradox: How Board Directors Must Navigate Hidden Energy Risks

The Edge Singapore featured my article on “Singapore's Energy Vulnerability Paradox: How Board Directors Must Navigate Hidden Energy Risks” on 3 July 2025.

Singapore's Energy Vulnerability Paradox: How Board Directors Must Navigate Hidden Energy Risks

In December 2022, Jinjja Chicken's managing director stared at an electricity bill that had quintupled to S$10,654 in a single month. His stark reaction—"there goes all my profit"—captured the existential reality facing Singapore businesses during the 2021-2022 energy crisis that destroyed six electricity retailers and forced cost increases across the economy that still remain today.

While Singapore appears remarkably resilient to energy shocks—academic research showing GDP actually increases by 0.96% when oil prices rise—this surface-level stability masks structural vulnerabilities that wipe-out profits within months.

For Singapore's board directors, the strategic challenge is not whether energy volatility affects their companies, but whether they understand the structural dependencies that transform manageable global risks into structural local threats requiring immediate governance intervention.

At First Glance: Singapore's Energy Trading Success

Singapore has established itself as a leading energy trading hub that initially suggests remarkable resilience to global energy volatility. The country traded approximately US$240 billion worth of LNG in 2022—equivalent to 50% of Singapore's GDP—despite producing no LNG domestically. As Asia's largest physical oil trading hub handling 25-35% of regional commodities trading, Singapore's petroleum manufacturing industry alone contributed S$9.48 billion in value-added in 2023, the highest among all manufacturing sectors.

The integrated complex on Jurong Island represents over S$50 billion in investments from nearly 100 companies, with the oil and petrochemical industry collectively accounting for around 4% of Singapore's GDP. During favorable market conditions, Singapore's refining margins demonstrate spectacular profit potential—touching record highs of $25.9 per barrel in Q2 2022, four times higher than from previous levels.

These impressive statistics create the compelling impression that Singapore benefits from oil price volatility rather than suffers from it, supported by academic research showing positive GDP correlation with oil price increases. For board directors reviewing these macro-economic indicators, the natural conclusion suggests energy risk management may be a lower priority than other business concerns.

The Hidden Reality: Structural Dependencies Create Systematic Risk

Beneath Singapore's impressive energy trading statistics lies a fundamentally different operational reality that creates multiple vulnerabilities across various sectors. Singapore imports approximately 95% of its energy needs, with natural gas being the primary source for electricity generation—one of the highest import dependency ratios globally. This near-total reliance on imported energy creates structural exposure to global market fluctuations that government reforms or risk management cannot eliminate.

In addition, Singapore's energy ecosystem operates through several critical single points of failure that amplify vulnerability beyond simple import dependence. The country currently operates only one LNG terminal supplying around half of its natural gas demand, while the remainder comes from pipeline gas from Indonesia and Malaysia. Recent episodes demonstrate the precarious nature of these arrangements: Sembcorp Industries terminated a gas sales agreement with Indonesian partners in March 2025 due to regulatory hurdles, forcing reliance on more expensive LNG alternatives.

Indonesia's shifting energy priorities compound these supply risks significantly. In May 2025, Energy minister Bahlil Lahadalia has called for Indonesia to stop oil imports from Singapore and buy directly from Middle East producers, while the country explicitly prioritizes domestic gas consumption over exports. This regional energy nationalism reflects broader trends that make Singapore's supply security increasingly precarious regardless of global energy price levels.

The 2021-2022 Crisis

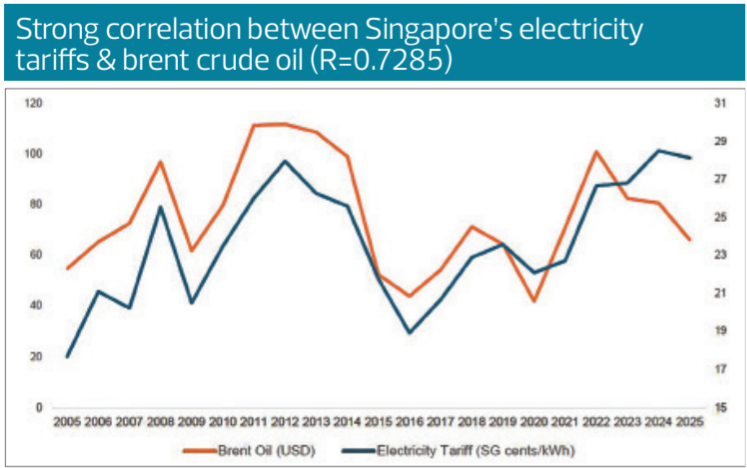

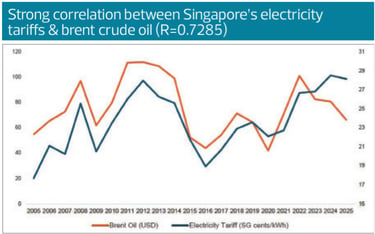

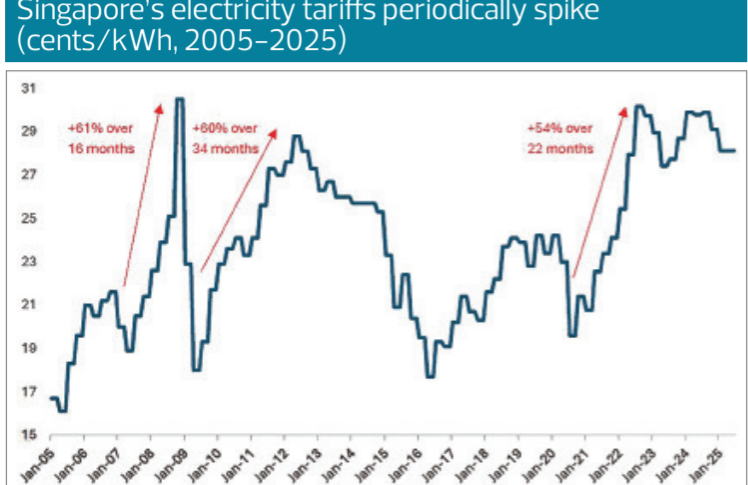

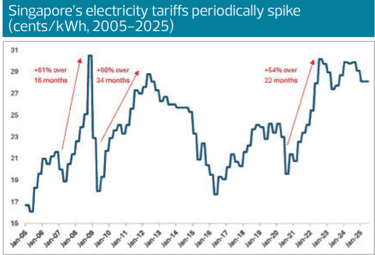

The 2021-2022 electricity crisis provides clear evidence of how Singapore's structural vulnerabilities rapidly transform from theoretical risks into business-threatening realities. Singapore's average wholesale electricity prices exploded from S$67 per megawatt hour in October 2020 to S$156/MWh in September 2021, reaching S$400/MWh during peak periods. This 500+% price spike upset established business models within weeks, forcing six electricity retailers to collapse entirely while another two prematurely terminated consumer contracts.

Approximately 140,000 households and 11,500 business accounts were affected, with some transferred to other retailers and others moved to SP Group. The Singapore Precision Engineering and Technology Association reported that 80% of approximately 2,700 electricity-intensive businesses faced significant impact, with many unable to absorb sudden cost increases. SMEs experienced electricity bill increases of three to five times their previous levels during crisis periods.

Manufacturing companies’ margins fell as utility cost increases contributed 0.9 percentage points to their unit business costs. The crisis revealed fundamental weaknesses in Singapore's electricity retail structure, where independent retailers lacking power plants must purchase electricity from spot markets, leaving them exposed to price spikes that reached 3,000% in some periods. In such a volatile market, even sophisticated hedging arrangements faced basis risk and counterparty exposure that overwhelmed protective strategies when wholesale prices increased 500% within week.

Sector-Specific Impact Assessment

Refining Sector Revenue Volatility

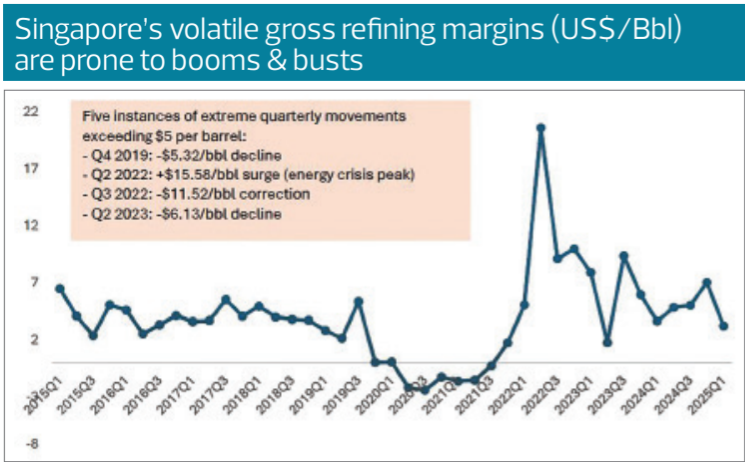

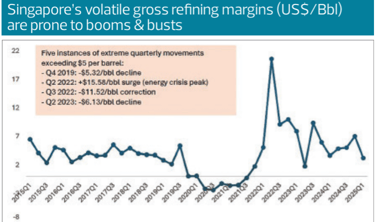

Singapore's refining sector demonstrates extreme vulnerability through gross refining margin compression (GRM) that contradicts conventional wisdom about oil price benefits. For the first nine months of 2024, Singapore's overall GRM averaged just $4.8 per barrel, representing a significant decrease from $7.2 per barrel in the same period of 2023 3. Historical analysis reveals dramatic volatility: Singapore GRMs averaged around $2.6 per barrel in Q4 2019, down 60% from the previous quarter and the lowest in 40 quarters.

When crude prices surge due to supply concerns rather than demand growth, refineries face devastating margin compression where input costs rise dramatically while product prices lag behind. For Singapore's refining sector processing 1.5 million barrels per day, even a modest $5 per barrel margin compression translates to $7.5 million in daily revenue reduction.

Industrial and Manufacturing Vulnerability

During the 2021-2022 crisis, industrial margins collapsed as energy costs contributed 0.9 percentage points to unit business costs. The 160 most energy-intensive firms consume 50% of industrial energy yet achieve only 0.7% annual efficiency gains—half the government's 1-2% target. This efficiency deficit creates a S$2.1 billion annual competitiveness disadvantage versus regional manufacturing hubs.

Data Center Existential Risk

Singapore's data center sector faces existential threats from energy constraints, with the country now ranked as the world's most power-constrained data center market having only 7.2 MW of available capacity and a record-low 1% vacancy rate. Data center construction costs have surged to US$13.80 per watt, making Singapore the second-most expensive globally. The Asia-Pacific data center market projected to reach US$28 billion by 2024 cannot be captured proportionally due to Singapore's energy constraints.

Financial Sector Systemic Exposure

The oil trading sector creates systemic risks extending beyond direct petroleum companies, as demonstrated by the Hin Leong collapse exposing 23 banks to significant losses. Singapore's major banks—DBS, OCBC, and UOB—faced $610 million in combined exposure to Hin Leong, while foreign banks including HSBC, ABN Amro, and Société Générale faced an additional $1.4 billion in exposure. The case revealed how oil price volatility creates conditions where trading losses escalate into massive fraud, described by PwC as "a vicious cycle" where financing requirements sustain fraudulent schemes.

Singapore-Specific Board Action Framework

Enhanced Hedging Strategy Implementation

Under Singapore's new regulatory framework, electricity retailers are required to hedge 80% of their contracted demand on rolling 24-month forward basis. Energy-intensive companies such as Singapore Airlines also hedge their fuel requirements to mitigate unexpected oil price hikes and reduce energy cost volatility.

However, boards must recognize the fundamental limitations of hedging strategies during extreme market conditions. The SGX electricity futures market launched in 2015 as Asia's first provides valuable risk management tools but demonstrated critical liquidity constraints during the 2021-2022 crisis when futures prices spiked above S$850/MWh, making hedging prohibitively expensive precisely when protection was most needed. Market participants report that "the futures market has zero liquidity" during crisis periods, representing complete breakdown of hedging mechanisms when most required.

Operational Resilience Planning

Boards should implement contingency planning for extended periods of elevated energy costs similar to the 2021-2022 experience, including operational scheduling to minimize peak-period consumption and strategic partnerships with energy service companies.

Directors must model quarterly tariff exposure scenarios, as energy costs (77% of total tariffs) automatically flow through within 90 days. Use the 2021-2022 baseline: wholesale prices jumping from S$67 to S$400/MWh represents 500% cost increases that eliminate profit margins overnight.

Manufacturing companies should review their operations and reduce their energy -intensive needs, where possible including implementing energy efficiency measures to achieve the government's target of 1-2% annual improvements needed to maintain competitiveness.

Crisis Communication and Stakeholder Management

Boards must establish crisis communication protocols addressing energy cost pass-through necessities during volatile periods, recognizing that Singapore's pricing mechanism makes cost absorption impossible for most companies. The systematic nature of cost transmission means businesses face impossible choices between absorbing unsustainable increases or passing them through to customers during market stress.

Directors should prepare scenario-based financial guidance helping stakeholders understand how different energy price levels affect business performance, including modeling electricity costs at S$400/MWh peaks experienced during the 2021-2022 crisis. Companies must quantify the impact of sustained high energy costs on cash flow, debt service capability, and competitive positioning within 90-day periods reflecting Singapore's quarterly tariff adjustment mechanism.

Conclusion: Managing Inevitable Structural Dependencies

The evidence demonstrates that Singapore's energy sector presents board directors with a fundamental governance challenge extending far beyond traditional risk management approaches. While the country's impressive energy trading statistics provide superficial comfort, the structural dependencies that enabled the 2021-2022 crisis remain largely unchanged, creating conditions where similar disruptions remain highly probable.

Singapore's 95% energy import dependence, concentrated supplier relationships, and systematic transmission of global market volatility through domestic pricing mechanisms create exposure that sophisticated risk management can mitigate but not eliminate. Government reforms including the Temporary Price Cap mechanism and Central Gas Entity provide valuable circuit breakers but offer limited protection during sustained high-price periods.

For Singapore's board directors, the strategic imperative requires transitioning from reactive crisis management to proactive risk positioning that acknowledges structural vulnerabilities while building competitive advantages through superior governance capabilities. The companies that thrive will be those whose boards recognize energy governance as equally critical to business survival as financial management, cybersecurity and regulatory compliance.

The choice is stark: implement sophisticated energy governance now, or explain to shareholders later why a quintupled electricity bill destroyed quarterly profits. Singapore's structural vulnerabilities guarantee the next crisis will come—the only question is whether boards will be prepared.

Written by:

Lee Ooi Keong

Ooi Keong is an independent board director of a SGX listed company with 30-years of experience in investments, corporate performance and governance. He is also the founder and MD of Clover Point Consultants -an independent Board and C-Suite advisory firm.

Like what you read? Follow me and read all my latest posts, articles and more!