Singapore's Stock Market Paradox: A Tale of Two Markets

The Edge Singapore featured my article "SINGAPORE'S STOCK MARKET PARADOX: A TALE OF TWO MARKETS" on 22 September 2025.

Singapore's Stock Market Paradox: A Tale of Two Markets

Singapore's Stock Market Paradox: A Tale of Two Markets

Singapore’s stock market is delivering impressive index-level returns. But behind the numbers lies a shrinking universe of listed companies, lackluster IPO activity and an exodus of growth startups and businesses. For board directors and senior executives, the contradiction isn’t just academic. It frames the future direction of Singapore’s capital markets and status as a leading financial hub.

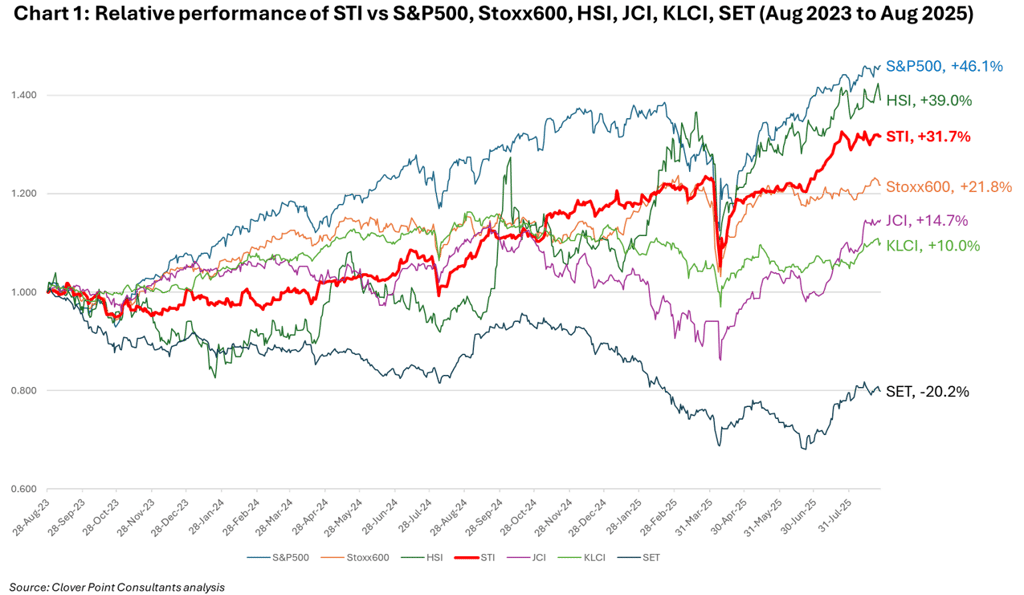

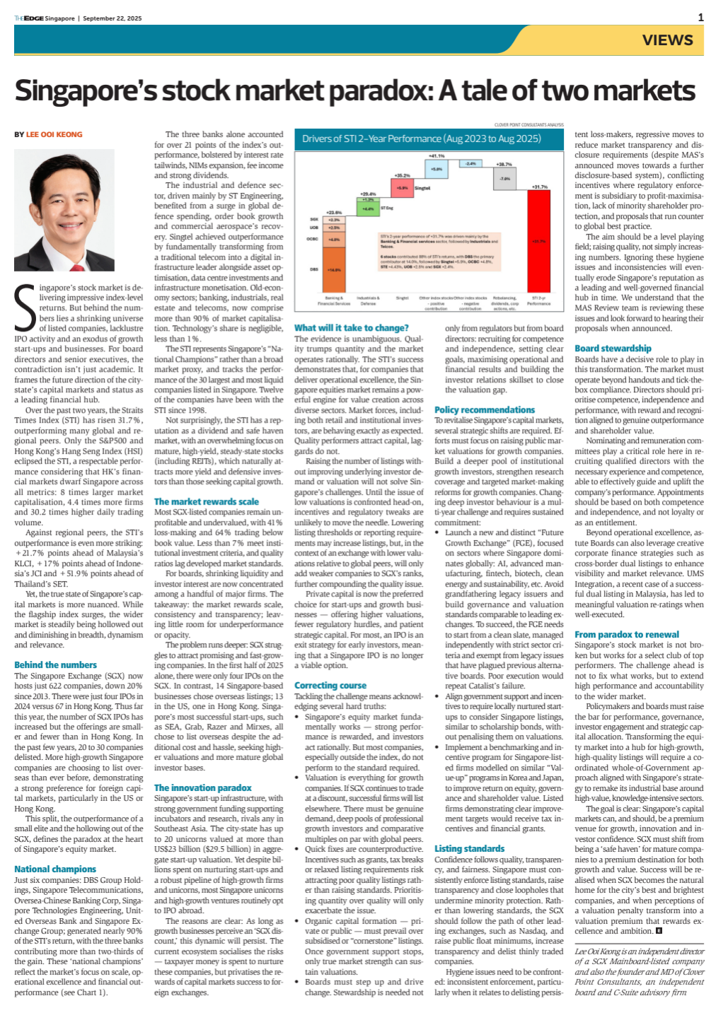

Over the past two years, the Straits Times Index (STI) has risen 31.7%, outperforming many global and regional peers. Only the S&P500 and Hong Kong’s Hang Seng Index (HSI) eclipsed the STI (see Chart 1), a respectable performance considering that HK’s financial markets dwarf Singapore across all metrics: 8.0x larger market capitalization, 4.4x more firms and 30.2x higher daily trading volume.

Against regional peers, the STI’s outperformance is even more striking: +21.7% points ahead of Malaysia's KLCI, +17.0% points ahead of Indonesia's JCI and +51.9% points ahead of Thailand's SET.

Yet, the true state of Singapore’s capital markets is more nuanced. While the flagship index surges, the wider market is steadily being hollowed out and diminishing in breadth, dynamism and relevance.

Behind the Numbers: Index Up, Market Down

SGX now hosts just 622 companies, down 20% since 2013. IPOs have slowed to a trickle, with four new listings in 2024 against 67 for Hong Kong. Each year, 20 to 30 companies delist. More high-growth Singapore companies are choosing to list overseas than ever before, demonstrating a strong preference for foreign capital markets, particularly in the US or Hong Kong.

This split, the outperformance of a small elite and the hollowing out of the SGX, defines the paradox at the heart of Singapore’s equity market.

Anatomy of Outperformance: National Champions

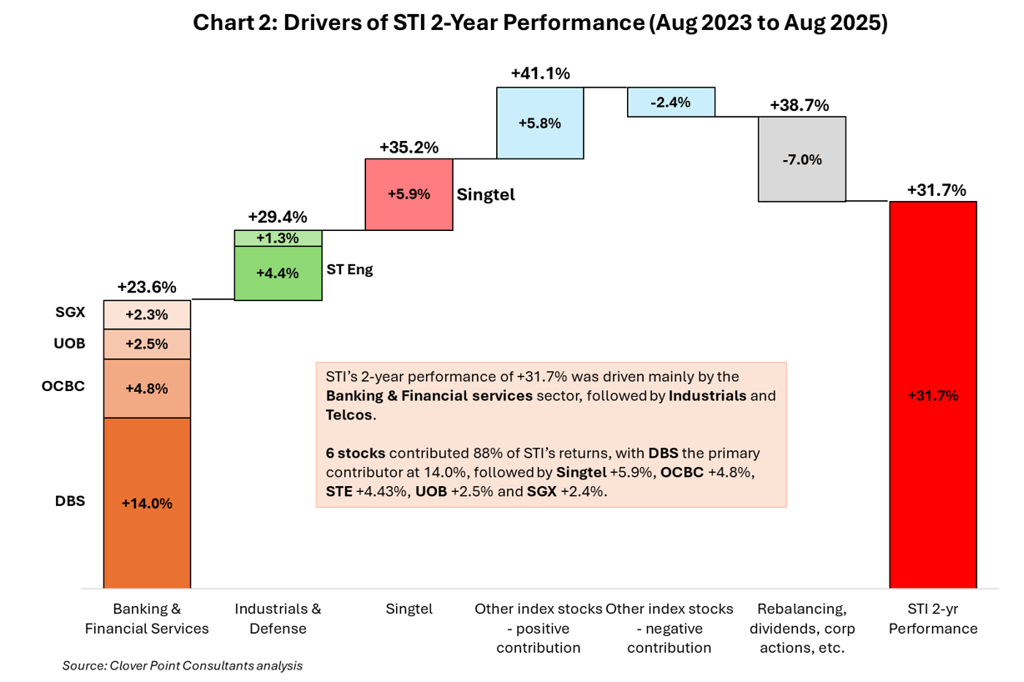

Just six companies: DBS, Singtel, OCBC, ST Engineering, UOB and SGX; generated nearly 90% of the STI’s return, with the three banks contributing more than two-thirds of the gain. These ‘national champions’ reflect the market’s focus on scale, operational excellence and financial outperformance (see Chart 2).

The three banks alone accounted for over 21 points of the index’s outperformance, bolstered by interest rate tailwinds, NIMs expansion, fee income and strong dividends.

The industrial and defense sector, driven mainly by ST Engineering, benefited from a surge in global defense spending, order book growth and commercial aerospace’s recovery. Singtel achieved outperformance by fundamentally transforming from a traditional telecom into a digital infrastructure leader alongside asset optimization, data center investments and infrastructure monetization.

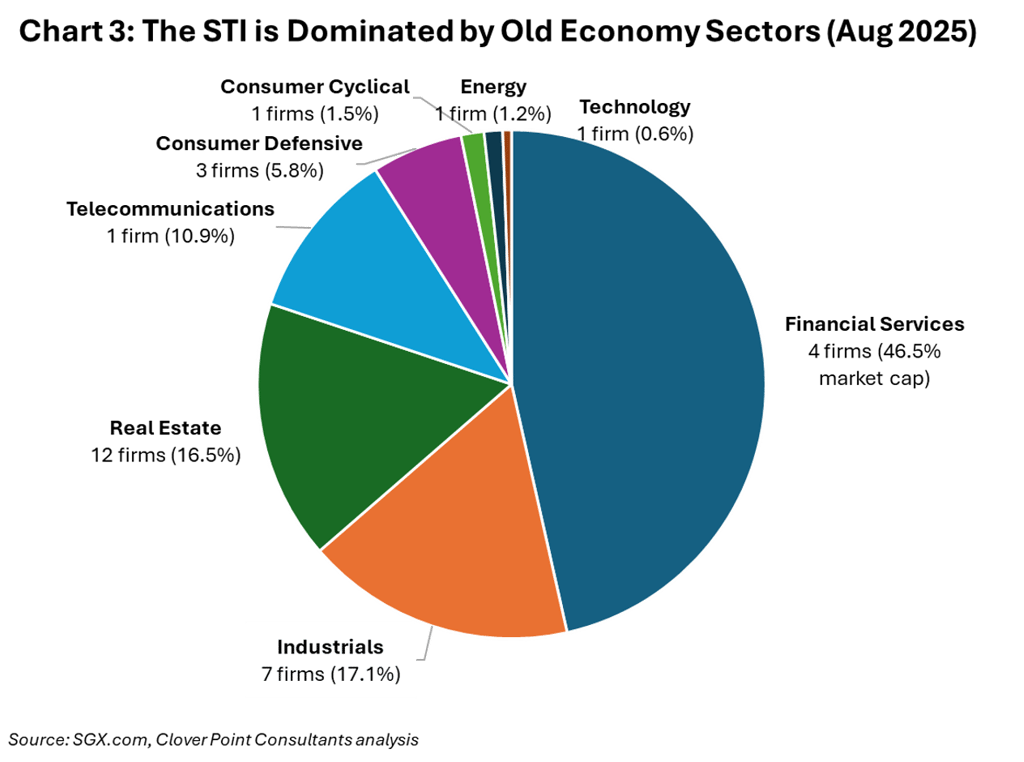

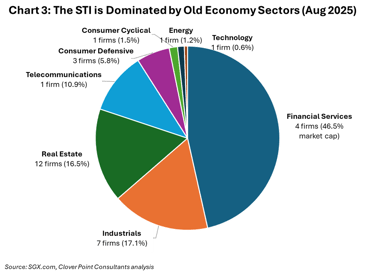

Old-economy sectors; banking, industrials, real estate and telecoms, now comprise more than 90% of market capitalization. Technology’s share is negligible, less than 1%.

The STI represents Singapore's "National Champions" rather than a broad market proxy, and tracks the performance of the 30 largest and most liquid companies listed in Singapore. 12 of the companies have been with the STI since 1998.

Hence, not surprisingly, the STI has a reputation as a dividend and safe haven market, with an overwhelming focus on mature, high-yield, steady-state stocks (including REITs), which naturally attracts more yield and defensive investors than those seeking capital growth.

While The Rest of SGX Struggles

Most SGX-listed companies remain unprofitable and undervalued, with 41% loss-making and 64% trading below book value. Less than 7% meet institutional investment criteria and quality ratios lag developed market standards.

For boards, shrinking liquidity and investor interest are now concentrated among a handful of major firms. The takeaway: the market rewards scale, consistency and transparency; leaving little room for underperformance or opacity.

The problem runs deeper: SGX struggles to attract promising and fast-growing companies. In the first half of 2025 alone, there were only four IPOs on the SGX. In contrast, 14 Singapore-based businesses chose overseas listings; 13 in the US, one in Hong Kong. Singapore’s most successful startups such as SEA, Grab, Razer and Mirxes all chose to list overseas despite the additional cost and hassle, seeking higher valuations and more mature global investor bases.

The Innovation Paradox: More Unicorns, Fewer IPOs

Singapore’s startup infrastructure with strong government funding supporting incubators and research rivals any in Southeast Asia. The city-state has up to 20 unicorns valued at more than US$23 billion in aggregate startup valuation. Yet despite billions spent on nurturing startups and a robust pipeline of high-growth firms and unicorns, most Singapore unicorns and high-growth ventures routinely opt to IPO abroad.

The reasons are clear: As long as growth businesses perceive a ‘SGX discount,’ this dynamic will persist. The current ecosystem socializes the risks – taxpayer money is spent to nurture these companies – but privatizes the rewards of capital markets success to foreign exchanges.

What Will It Take to Change?

The evidence is unambiguous. Quality trumps quantity.

The market operates rationally. The STI's success demonstrates that, for companies that deliver operational excellence, the Singapore equities market remains a powerful engine for value creation across diverse sectors. Market forces, including both retail and institutional investors, are behaving exactly as expected. Quality performers attract capital, laggards do not.

Raising the number of listings without improving underlying investor demand or valuation will not solve Singapore’s challenges. Until the issue of low valuations is confronted head-on, incentives and regulatory tweaks are unlikely to move the needle. Lowering listing thresholds or reporting requirements may increase listings but, in the context of an exchange with lower valuations relative to global peers, will only add weaker companies to SGX’s ranks, further compounding the quality issue.

Private capital is now the preferred choice for startups and growth businesses – offering higher valuations, fewer regulatory hurdles, and patient strategic capital. For most, an IPO is an exit strategy for early investors, meaning that a Singapore IPO is no longer a viable option.

Correcting Course: The Way Forward

Tackling the challenge means acknowledging several hard truths:

Singapore’s equity market fundamentally works – strong performance is rewarded, and investors act rationally. But most companies, especially outside the index, do not perform to the standard required.

Valuation is everything for growth companies. If SGX continues to trade at a discount, successful firms will list elsewhere. There must be genuine demand, deep pools of professional growth investors and comparative multiples on par with global peers.

Quick fixes are counterproductive. Incentives such as grants, tax breaks or relaxed listing requirements risk attracting poor quality listings rather than raising standards. Prioritizing quantity over quality will only exacerbate the issue.

Organic capital formation – private or public – must prevail over subsidized or “cornerstone” listings. Once government support stops, only true market strength can sustain valuations.

Boards must step up and drive change. Stewardship is needed not only from regulators but from board directors: recruiting for competence and independence, setting clear goals, maximizing operational and financial results and building the investor relations skillset to close the valuation gap.

Policy Recommendations for Renewal

To revitalize Singapore’s capital markets, several strategic shifts are required:

Efforts must focus on raising public market valuations for growth companies. Build a deeper pool of institutional growth investors, strengthen research coverage and targeted market-making reforms for growth companies. Changing deep investor behavior is a multi-year challenge and requires sustained commitment.

Launch a new and distinct “Future Growth Exchange” (FGE), focused on sectors where Singapore dominates globally; AI, advanced manufacturing, fintech, biotech, clean energy and sustainability, etc. Avoid grandfathering legacy issuers and build governance and valuation standards comparable to leading exchanges. To succeed, the FGE needs to start from a clean slate, managed independently with strict sector criteria and exempt from legacy issues that have plagued previous alternative boards. Poor execution would repeat Catalist’s failure.

Align government support and incentives to require locally nurtured startups to consider Singapore listings, similar to scholarship bonds, without penalizing them on valuations.

Implement a benchmarking and incentive program for Singapore listed firms modeled on similar “Value-up” programs in Korea and Japan, to improve return on equity, governance and shareholder value. Listed firms demonstrating clear improvement targets would receive tax incentives and financial grants.

Addressing Hygiene Issues and Inconsistencies

Confidence follows quality, transparency, and fairness. Singapore must consistently enforce listing standards, raise transparency and close loopholes that undermine minority protection. Rather than lowering standards, the SGX should follow the path of other leading exchanges, such as Nasdaq, and raise public float minimums, increase transparency and delist thinly traded companies

Hygiene issues need to be confronted: inconsistent enforcement particularly when it relates to delisting persistent loss-makers, regressive moves to reduce market transparency and disclosure requirements (despite MAS’ announced moves towards further disclosure-based system), conflicting incentives where regulatory enforcement is subsidiary to profit-maximization, lack of minority shareholder protection, and proposals that run counter to global best practice.

The aim should be a level playing field; raising quality, not simply increasing numbers. Ignoring these hygiene issues and inconsistencies will eventually erode Singapore’s reputation as a leading and well-governed financial hub in time.

We understand that the MAS Review team is reviewing these issues and look forward to hearing their proposals when announced.

Board Stewardship

Boards have a decisive role to play in this transformation. The market must operate beyond handouts and tick-the-box compliance. Directors should prioritize competence, independence and performance, with reward and recognition aligned to genuine outperformance and shareholder value.

Nominating and Remuneration Committees play a critical role here in recruiting qualified directors with the necessary experience and competence able to effectively guide and uplift company performance. Appointments should be based on both competence and independence, and not loyalty or as an entitlement.

Beyond operational excellence, astute Boards can also leverage creative corporate finance strategies such as cross-border dual listings to enhance visibility and market relevance. Recent successful dual listings, notably Grand Venture Technology and UMS Integration, in Malaysia have led to meaningful valuation re-ratings where well-executed.

Conclusion: From Paradox to Renewal

Singapore’s stock market is not broken but works for a select club of top performers. The challenge ahead is not to fix what works, but to extend high performance and accountability to the wider market.

Policymakers and boards must raise the bar for performance, governance, investor engagement and strategic capital allocation. Transforming the equity market into a hub for high-growth, high-quality listings will require coordinated whole-of-Government approach aligned with Singapore’s strategy to remake its industrial base around high-value, knowledge-intensive sectors.

The goal is clear: Singapore’s capital markets can, and should, be a premium venue for growth, innovation and investor confidence. SGX must shift from being a ‘safe haven’ for mature companies to a premium destination for both growth and value. Success will be realized when SGX becomes the natural home for the city’s best and brightest companies, and when perceptions of a valuation penalty transform into a valuation premium that rewards excellence and ambition.

Written by:

Lee Ooi Keong

Brief bio: Lee Ooi Keong is an Independent Director of a SGX Mainboard-listed company with 30-years of experience in corporate performance, investments and risk management. He is also the founder and MD of Clover Point Consultants – an independent Board and C-Suite advisory firm.

Like this article? Follow me on Linkedin and read my latest posts, articles and more!