Independent Board Advisory, Training and Professional Speaking

The Geopolitical Illusion: Why "Forecasting Geopolitics"Is Poor Risk Management

The Edge Singapore featured my article THE GEOPOLITICAL RISK ILLUSION: Why Forecasting Geopolitics Is Poor Risk Management on 10 November 2025.

Lee Ooi Keong

11/26/20255 min read

The Geopolitical Risk Illusion: Why “Forecasting Geopolitics” Is Poor Risk Management

TLDR version. Full version.

The Prediction Trap

Singapore companies have spent millions on geopolitical dashboards, scenario planning exercises, early‑warning AI tools and geopolitical consulting services. Yet none predicted or prevented losses from COVID‑19, Russia’s invasion of Ukraine or Middle Eastern conflicts. The failure was not lack of information – it was poor design.

A growing body of evidence shows most are solving the wrong problem. Analysis of 88 major geopolitical crises since 1931 and IMF, World Bank and BlackRock studies confirm market outcomes are rarely shaped by geopolitics. Companies that outperform don’t predict better, they prepare better.

What the Data Shows

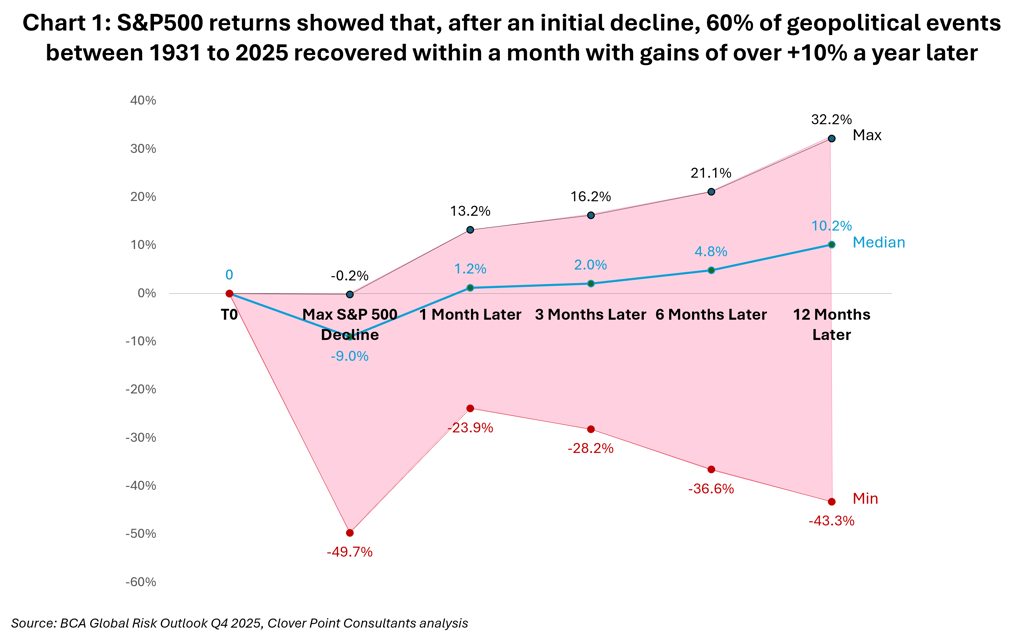

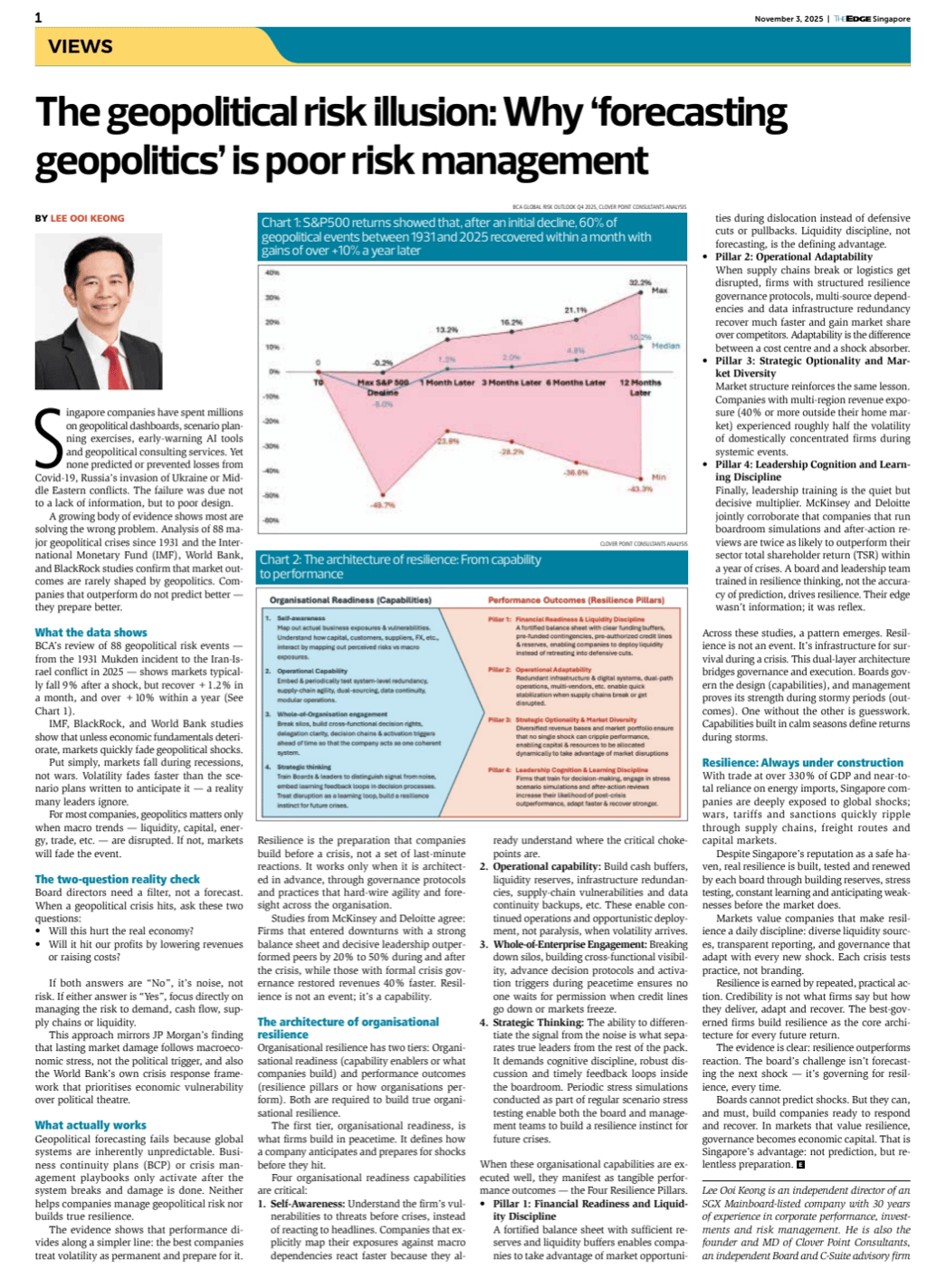

BCA’s review of 88 geopolitical risk events – from the 1931 Mukden incident to the Iran-Israel conflict in 2025 – shows markets typically fall 9% after a shock, but recover +1.2% in a month, and over +10% within a year. (See Chart 1)

IMF, BlackRock and World Bank studies show that unless economic fundamentals deteriorate, markets quickly fade geopolitical shocks.

Put simply, markets fall during recessions, not wars. Volatility fades faster than the scenario plans written to anticipate it – a reality many leaders ignore.

For most companies, geopolitics matters only when macro trends – liquidity, capital, energy, trade, etc. – are disrupted. If not, markets will fade the event.

The Two Question Reality Check

Board directors need a filter, not a forecast.

When a geopolitical crisis hits, ask:

Will this hurt the real economy?

Will it hit our profits by lowering revenues or raising costs?

If both answers are “No”, it’s noise – not risk. If either answer is “Yes”, focus directly on managing the risk to demand, cash flow, supply chains or liquidity.

This approach mirrors J.P. Morgan’s finding that lasting market damage follows macroeconomic stress, not the political trigger, and also the World Bank’s own crisis response framework that prioritises economic vulnerability over political theatre.

What Actually Works

Geopolitical forecasting fails because global systems are inherently unpredictable. Business Continuity Plans (BCP) or crisis management playbooks only activate after the system breaks and damage is done. Neither helps companies manage geopolitical risk nor builds true resilience.

The evidence shows that performance divides along a simpler line: the best companies treat volatility as permanent and prepare for it. Resilience is the preparation that companies build before a crisis, not a set of last-minute reactions. It works only when it’s architected in advance, through governance protocols and practices that hard‑wire agility and foresight across the organisation.

Studies from McKinsey and Deloitte agree: Firms that entered downturns with strong balance sheet and decisive leadership outperformed peers by 20% to 50% during and after the crisis, while those with formal crisis governance restored revenues 40% faster. Resilience is not an event, it’s a capability.

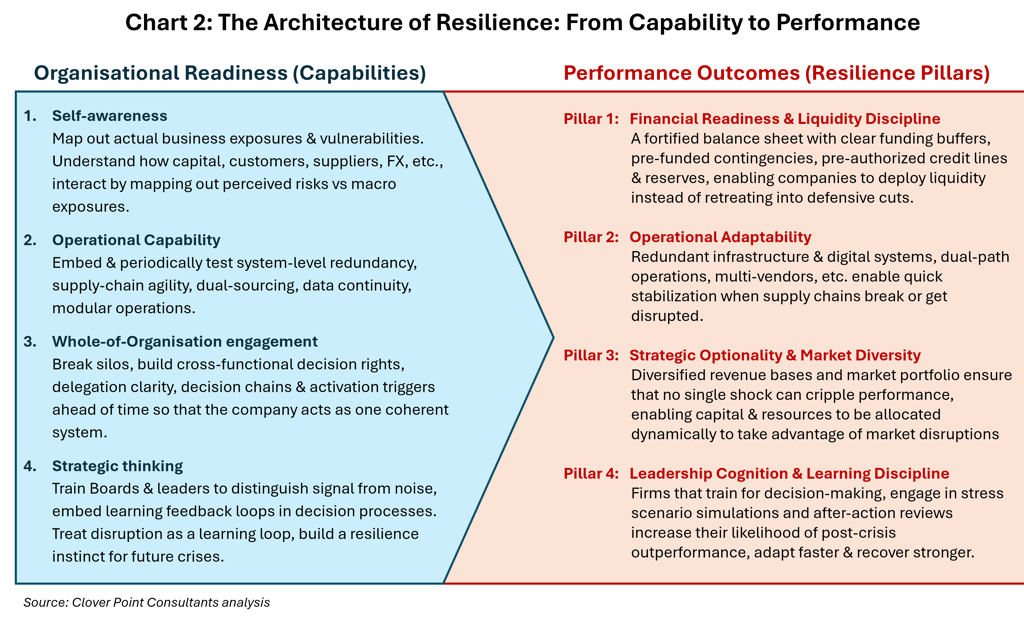

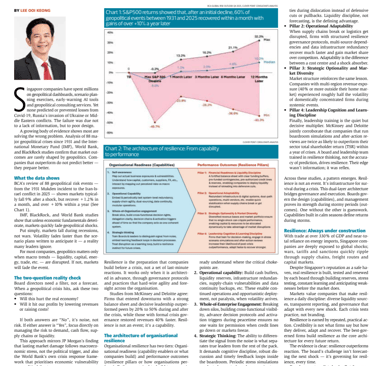

The Architecture of Organisational Resilience

Organisational resilience has two tiers: Organisational readiness (capability enablers or what companies build) and Performance outcomes (resilience pillars or how organisations performs), both of which are required to build true organisational resilience.

The first tier, Organisational readiness, is what firms build in peacetime. It defines how a company anticipates and prepares for shocks before they hit.

Four organisational readiness capabilities are critical:

Self‑Awareness: Understand the firm’s vulnerabilities to threats before crises, instead of reacting to headlines. Companies that explicitly map their exposures against macro dependencies react faster because they already understand where the critical chokepoints are.

Operational capability: Build cash buffers, liquidity reserves, infrastructure redundancies, supply-chain vulnerabilities and data continuity backups, etc. These enable continued operations and opportunistic deployment, not paralysis, when volatility arrives.

Whole‑of‑Enterprise Engagement: Breaking down silos, building cross‑functional visibility, advance decision‑protocols and activation triggers during peace time ensure no one waits for permission when credit lines go down or markets freeze.

Strategic Thinking: The ability to differentiate the signal from the noise is what separates true leaders from the rest of the pack. It demands cognitive discipline, robust discussion and timely feedback loops inside the boardroom. Periodic stress simulations conducted as part of regular scenario stress testing enable both board and management teams to build a resilience instinct for future crises.

When these organisational capabilities are executed well, they manifest as tangible performance outcomes – the Four Resilience Pillars.

Pillar 1: Financial Readiness and Liquidity Discipline

A fortified balance sheet with sufficient reserves and liquidity buffers enable companies to take advantage of market opportunities during dislocation instead of defensive cuts or pullbacks. Liquidity discipline, not forecasting, is the defining advantage.

Pillar 2: Operational Adaptability

When supply chains break or logistics gets disrupted, firms with structured resilience governance protocols, multi-source dependencies and data infrastructure redundancy recover much faster and gain market share over competitors. Adaptability is the difference between a cost centre and a shock absorber.Pillar 3: Strategic Optionality and Market Diversity

Market structure reinforces the same lesson. Companies with multi-region revenue exposure (40% or more outside their home market) experienced roughly half the volatility of domestically concentrated firms during systemic events.

Pillar 4: Leadership Cognition and Learning Discipline

Finally, leadership training is the quiet but decisive multiplier. McKinsey and Deloitte jointly corroborate that companies that run boardroom simulations and after-action reviews are twice as likely to outperform their sector total shareholder return (TSR) within a year of crises. A board and leadership team trained in resilience thinking, not accuracy of prediction, drives resilience. Their edge wasn’t information – it was reflex.

Across these studies, a pattern emerges. Resilience is not an event. It’s infrastructure for survival during crisis. This dual-layer architecture bridges governance and execution. Boards govern the design (capabilities), management proves its strength during stormy periods (outcomes). One without the other is guesswork. Capabilities built in calm seasons define returns during storms.

Resilience: Always Under Construction

With trade at over 330% of GDP and near-total reliance on energy imports, Singapore companies are deeply exposed to global shocks; wars, tariffs and sanctions quickly ripple through supply chains, freight routes and capital markets.

Despite Singapore’s reputation as a safe haven, real resilience is built, tested and renewed by each board – through building reserves, stress testing, constant learning and anticipating weaknesses before the market does.

Markets value companies that make resilience daily discipline: diverse liquidity sources, transparent reporting, and governance that adapt with every new shock. Each crisis tests practice, not branding.

Resilience is not a slogan – it’s earned by repeated, practical action. Credibility isn’t what firms say but how they deliver, adapt and recover. The best-governed firms build resilience as the core architecture for every future return.

The evidence is clear: resilience outperforms reaction. The board’s challenge isn’t forecasting the next shock – it’s governing for resilience, every time.

Boards can’t predict shocks. But they can, and must, build companies ready to respond and recover. In markets that value resilience, governance becomes economic capital. That is Singapore’s advantage: not prediction, but relentless preparation.

Written by:

Lee Ooi Keong

28 October 2025

Brief bio: Lee Ooi Keong is an Independent Director of a SGX Mainboard-listed company

with 30-years of experience in corporate performance, investments and risk management. He is also the founder and MD of Clover Point Consultants – an independent Board and C-Suite advisory firm.